When discussing retirement plans, we utilize a communication tool called the Personal Economic Model®. Similar to how a medical doctor uses an anatomical model to explain medical concepts, we use this model to explain financial concepts.

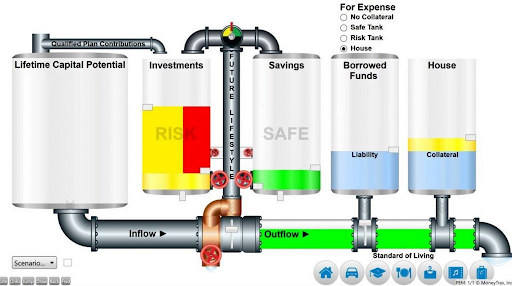

The Personal Economic Model® is a communication tool we use to illustrate financial concepts related to retirement planning. This model provides a visual representation of how money flows through your hands. On the left side, you will see the Lifetime Capital Potential tank, which represents all the money you will earn during your lifetime. This amount is substantial but also finite. After earning the money, it flows directly to the Tax Filter where state and federal governments extract tax dollars from your monthly cash flow. The remaining after-tax balance is then allocated to either your Current Lifestyle or your Future Lifestyle, which is determined by your management of the Lifestyle Regulator. Deciding the balance of cash flow between your current lifestyle desires and your future lifestyle needs is a crucial financial decision.

Here’s why:

Every dollar that you spend on your Current Lifestyle is gone forever. The objective is to save enough money in the Savings and Investment tanks so that when you retire, you can use the funds to fulfill your future lifestyle requirements. The ideal scenario is to have enough savings to live like you do today adjusted for inflation and have your money last until your life expectancy. This is a great achievement, but it’s even better if you can accomplish it without compromising your current standard of living, and that’s what we aim to assist our clients to do. By collaborating with us, we can assist you in:

- Balancing your Current and Future Lifestyles effectively

- Enhancing the efficiency of your current personal economic model

- Developing and executing a plan to secure your financial future

- Limiting the impact on your Current Lifestyle funds (maintaining your existing standard of living)